Operator Hypotheses #3: Chai Discovery

Testing how early execution decisions constrain later strategic choices (in drug discovery AI).

Started: December 2025 (Month 21 post-founding, Month 14 post-seed)

Check back: October 2026

Confidence Level: 60-70% (multiple forks cascading with external dependencies)

About This Series

Operator Hypotheses tests whether execution forks in startups are predictable from public data. Each entry tracks one company over 12 months to see if repeatable patterns appear at predictable times.

Pattern #3 examines compound fork effects: how early execution decisions constrain later strategic choices in drug discovery AI. This extends Pattern #1’s (Research Grid) single-fork analysis to demonstrate how multiple forks cascade, with each decision constraining the next.

Chai is ~21 months post-founding, the window where GTM patterns become observable but multiple variables remain in motion. This timing means predictions have 60-70% confidence—higher than speculation, lower than the 85-95% certainty possible for earlier architectural decisions.

See Pattern #0 for the complete framework.

The Fork That Breaks Companies

In March 2025, BenevolentAI was delisted from the London Stock Exchange. Seven years earlier, the company had raised hundreds of millions in venture capital to build AI for drug discovery. At its peak, the market valued it at $2.4 billion. By delisting, it was down 99% and forced to abandon its hybrid model—the strategy of running both a platform business and an internal drug pipeline.

This wasn’t market conditions or bad luck. This was compound forks.

In 2018, BenevolentAI made one decision: pursue commercial partnerships with pharma companies before building deep academic credibility. That choice locked in a sequence. Pharma treated them as vendors, not research collaborators. Vendors get asked for custom integration work. Custom work creates the services trap—engineering time spent on per-customer branches instead of platform development. Services revenue funded an internal clinical pipeline. The hybrid model required continuous capital raises. When the clinical programs didn’t advance fast enough, the company collapsed.

Seven years. One initial fork. An irreversible cascade.

Compare that to Isomorphic Labs. DeepMind spun out Isomorphic in 2021, after publishing the breakthrough AlphaFold work that won the Nobel Prize in Chemistry. Academic credibility came first. When Isomorphic signed partnerships, pharma treated them as research peers, not vendors. The terms were different: $1.7 billion with Eli Lilly, $1.2 billion with Novartis—platform access deals, not per-target services contracts. No services trap. No capital crunch. In 2024, they raised a $600M Series A on the strength of their research platform. They can afford selective internal programs because platform economics came first.

The difference wasn’t the science. Both companies had world-class AI models. Both had experienced teams. Both were positioned at the same constraint: AI had made drug discovery faster, but clinical development was still slow and expensive.

The difference was Fork #1.

Chai Discovery is standing at that exact fork right now.

Why Chai

Chai Discovery is worth tracking because they’re entering Fork #1 at exactly the moment when it matters most and we can see the decision in real time.

The technology is credible: near-20% hit rates on de novo antibody design, roughly double industry baselines. The team is strong: experienced founders who understand both AI and drug discovery. The timing looks right: AI has made drug discovery faster, creating bottlenecks in clinical development that Chai’s platform addresses. The $70M Series A led by Menlo Ventures, with Mikael Dolsten (former Pfizer CSO) joining the board, suggests serious institutional backing.

But seven other drug discovery AI companies had similar advantages. Four collapsed or remain under severe strain. Only one succeeded—with Alphabet’s backing. Two are stable by staying platform-focused.

Chai is at Month 21. The first major partnerships are closing now. The contracts being negotiated in Q4 2025 and Q1 2026 will lock in data ownership terms that determine everything that follows. If they choose academic credibility over commercial velocity, the services trap probably won’t trigger. If they choose commercial velocity, it very likely will.

This is the crucible moment. We can watch it happen, predict the path, and check back in 12 months to see if compound forks are predictable from public signals.

Fork #1: Will pharma treat you as a peer or a vendor?

This first fork is simple: do you lean into publishing and scientific reputation, or into closing deals and growing revenue?

Chai has working models. Chai-1 and Chai-2 show a near-20% hit rate on fully de novo antibody design—roughly double industry baselines. They raised a $70M Series A in August 2025, led by Menlo Ventures. Mikael Dolsten, Pfizer’s former Chief Scientific Officer, joined their board. The technology works. The team is credible. The market timing looks right.

The next six months determine whether they prioritize:

Path A: Academic credibility → Publish major papers, open-source model components, build scientific reputation through peer review and independent validation.

Path B: Commercial velocity → Sign pharma partnerships, close paying customers, grow revenue as fast as possible.

This isn’t about ego or prestige. It’s about how pharma companies position you in their procurement and R&D workflows.

Academic-first companies get treated as collaborators. Pharma invites them to co-author papers, includes them in scientific advisory boards, offers non-exclusive platform access deals, and gives them latitude to publish findings and retain aggregate data rights. The relationship is peer-to-peer.

Commercial-first companies get treated as vendors. Procurement teams manage the relationship. Contracts request exclusive rights by default. Custom integration demands come early. Data ownership terms get negotiated heavily in pharma’s favor. The relationship is transactional.

The same pharmaceutical company will treat the same technology completely differently based on this single perception.

The Evidence: Seven Companies, Two Paths

I analyzed every major drug discovery AI company—public or well-funded private—to see if this pattern holds. Seven companies total. Small sample, but it’s nearly the entire category.

Academic-first path:

Isomorphic Labs (Alphabet/DeepMind spinout, 2021) - Published AlphaFold foundation work, signed $2.9B in platform partnerships (Lilly, Novartis), raised $600M Series A. Status: Stable, high-value partnerships, no services trap.

Schrödinger (Founded 1990, IPO 2020) - Published 350+ peer-reviewed papers before heavy commercial push. Software revenue is majority (~70% gross margins). Status: Public, $2.4B market cap, platform-dominant model working.

Commercial-first path:

BenevolentAI (Founded 2013, IPO 2021, delisted March 2025) - Signed early commercial partnerships (GSK, AstraZeneca, 2018-2020), built 20+ internal programs, pursued hybrid model. Status: Down 99%, delisted, forced to abandon hybrid and retreat to platform.

Recursion Pharmaceuticals (Founded 2013, IPO 2021) - Started platform-first, then added internal pipeline. Runs 10+ internal programs plus 10+ partnerships. Status: Public but cut programs in 2025; hybrid model under strain.

Atomwise (Founded 2012) - Commercial partnerships early, 13 years in, no clinical trials yet. New CEO hired February 2025 specifically to push internal candidates forward. Status: Struggling with transition to hybrid.

Insilico Medicine (Founded 2014) - Filed for Hong Kong IPO but never listed, raised $110M Series E instead. Burning cash on hybrid model. Status: Best-case hybrid outcome still requires continuous external capital.

Absci (Founded 2011, IPO 2021) - Pure platform play, no internal pipeline. Milestone payments and royalties from manufacturers. Status: Public, but partnership revenue alone hasn’t delivered venture-scale growth.

Pattern recognition:

Academic-first (2 companies): Both stable. One spectacularly successful with Alphabet backing. Platform-dominant revenue models.

Commercial-first into hybrid (4 companies): All struggling or failed. BenevolentAI collapsed. Recursion, Atomwise, Insilico all show strain.

Pure platform (1 company): Stable but hasn’t reached venture-scale growth.

The causal mechanism: Academic credibility shapes partnership terms → partnership terms determine services trap exposure → services trap outcome constrains later strategic options.

Chai’s Current Position

Chai is showing both signals right now.

Academic signals:

Released Chai-1 model via bioRxiv preprint in October 2024

Open-sourced portions of the technology

Building scientific credibility through technical disclosure

Commercial signals:

$70M Series A suggests investor pressure for revenue

Mikael Dolsten on board likely facilitates pharma introductions

Month 14-20 post-seed is typical timing for first major commercial deals

Dolsten’s presence tilts perception toward commercial readiness, but their publication cadence still signals scientific intent.

The fork is happening now. The structure of the next partnership Chai signs will reveal which path they’ve chosen.

Academic credibility or commercial velocity. Collaborator or vendor. This decision determines whether the three forks that follow even appear—and if they do, whether Chai can navigate them.

Fork #4: The invisible clause that decides the next three years

This fork doesn’t appear in press releases. It’s decided in contract terms during the first major pharma partnership—typically Month 15-20, between Fork #1 and Fork #2.

Most companies don’t realize this is a fork at all. It feels like standard contract negotiation: pharma’s legal team requests exclusive rights to antibody designs, training data and results. The language seems reasonable—they’re paying for the work, they want to own what’s produced.

But this clause determines everything that follows.

The Hidden Decision

Path A: Partner retains exclusive rights

Pharma owns all antibody designs generated for their targets

Chai cannot use learnings from Partner X’s projects for Partner Y

Each new partnership starts from scratch

No cross-customer learning, no compounding platform advantages

This is de facto per-customer customization, even if it’s not called “services”

Path B: Chai retains aggregate learning rights

De-identified data flows back to improve base models

Each partnership makes the platform better for everyone

Network effects compound over time

True platform economics become viable

The contract language that creates Path A looks like this:

“Exclusive rights to all antibodies designed for Target Library X”

“Custom-trained models for Partner Y’s proprietary data”

“Partner retains all intellectual property generated during collaboration”

The contract language that creates Path B looks like this:

“Non-exclusive platform access”

“Chai retains rights to de-identified aggregate learnings”

“Joint publications of methodological advances”

“Compute/API-based pricing” (not per-target licensing)

Why This Is Invisible But Critical

Data ownership determines whether you’re building a platform or running a consulting business with a software wrapper.

With aggregate learning rights (Path B):

Partnership #1 trains your models on oncology targets

Partnership #2 benefits from those learnings for immunology targets

Partnership #3 gets an even better platform

Each deal makes you more valuable to the next customer

This is what “platform effects” actually means

Without aggregate learning rights (Path A):

Partnership #1 produces custom models that stay in a silo

Partnership #2 requires building from scratch

Partnership #3 is no easier than Partnership #1

You’re rebuilding custom solutions for each customer

This is what “services trap by another name” looks like

The Evidence From Drug Discovery AI

We saw this pattern across the seven companies:

Isomorphic Labs signed partnerships that allowed them to publish methodological advances and retain platform learning rights. Each deal improved their base models. The $2.9B in partnership value reflects platform access, not per-target work.

BenevolentAI’s early partnerships (GSK, AstraZeneca) included exclusive rights clauses. They couldn’t use learnings from one pharma partner to improve work for another. This locked them into per-customer customization years before the services revenue numbers made it obvious.

The hidden fork created the visible trap.

How to Detect It (From Outside)

Since contracts aren’t public, you have to infer data ownership from secondary signals:

Exclusive rights indicators:

“Dedicated to Partner X’s therapeutic areas”

“Exclusive collaboration in oncology” (or any specific indication)

Per-target or per-molecule licensing structure

No mention of publications or shared learning

Aggregate learning indicators:

“Non-exclusive research collaboration”

“Platform access agreement”

Explicit joint publication clauses

Multiple partnerships in overlapping therapeutic areas (suggests shared learning)

Compute/API-based pricing rather than per-target fees

Partnership announcements rarely state data ownership explicitly, but the surrounding language reveals the structure.

The Compound Effect

Fork #4 sits between Fork #1 and Fork #2 chronologically, but it’s causally linked to both:

Fork #1 (Academic vs Commercial) determines Fork #4:

Academic credibility → pharma treats you as peer → negotiates shared learning rights from position of strength

Commercial velocity → pharma treats you as vendor → demands exclusive rights as standard practice

Fork #4 (Data Ownership) determines Fork #2:

Shared learning rights → platform can compound → services trap avoidable with discipline

Exclusive rights → no cross-customer learning → services trap becomes inevitable

For Chai, this fork is being decided right now in the terms of their first major partnerships. The clauses being negotiated in Q4 2025 and Q1 2026 will constrain every decision that follows.

The invisible fork locks in the path.

Fork #2: The phone call that looks like revenue but acts like gravity

If Chai takes the commercial-first path at Fork #1, this moment arrives between Month 18-24. Very likely, not certain—but the pattern is consistent enough that you can almost script it.

A pharma partner calls. They’ve been using Chai’s platform for six months and the results are strong. They want to expand usage across more therapeutic areas and extend the contract. There’s one request: they need a custom connector to their internal trial management system.

The integration is technically straightforward. The partner has already budgeted for it—call it $250K in additional annual revenue. The sales team forwards the request with a note: “This unlocks the full expansion. High confidence close if we can deliver by Q2.”

This is the moment. Say yes, and the integration that’s scoped at six weeks takes four months. The partner sees you did custom work and asks for more. Another partner hears about it and requests their own integration. By Month 24, three engineers are maintaining partner-specific code branches instead of improving the core platform.

Why It’s a Trap

The economics break systematically:

Platform revenue: 75-85% gross margins. Build once, sell to everyone. Each new customer makes the product better through aggregate learnings.

Services revenue: 20-35% gross margins. Build for one customer, maintain it forever. Each new customer requires dedicated engineering time.

When blended gross margins drop below 65%, investors reclassify you from “software” to “services.” Valuation multiples compress by roughly 50%—from 12-18x ARR to 6-10x ARR. Exit trajectories cap at strategic acquisitions to consulting firms rather than category-defining outcomes.

The strategic damage compounds:

Product roadmap slips (engineers diverted to custom work)

Platform differentiation erodes (custom work is commoditized)

Engineering morale suffers (maintaining custom branches is repetitive)

Talent leaves (best engineers want to work on hard platform problems)

More services work fills the gap (creating a death spiral)

The Evidence

Companies that avoided the trap kept services revenue minimal and ran it at deliberately unprofitable margins:

Snowflake: Services <6% of revenue, operated at -34% margins—intentionally unprofitable to discourage growth.

UiPath: Services <5% of revenue, also deliberately unprofitable.

Schrödinger: Software represents ~70% of revenue with strong margins; drug discovery services (higher-touch) is the minority segment.

As the BenevolentAI collapse showed, accepting early customization requests leads directly to services revenue growth, which funds hybrid model thinking, which creates unsustainable capital requirements.

How to Detect It

The services trap doesn’t announce itself. Look for these signals:

Partnership language: “Exclusive rights to Partner X’s targets,” “dedicated team,” “custom models,” “per-target licensing”—these indicate per-customer customization, not platform scaling.

Hiring patterns: “Professional Services Manager,” “Forward Deployed Engineer,” “Customer Success Engineer” roles suggest services organization buildout.

Revenue mix: If services/implementation revenue exceeds 15% and is growing faster than platform revenue, the trap is active.

Engineering allocation: If more than 20% of engineering time goes to customer-specific work, platform velocity will suffer.

Product cadence: Major releases slipping or gaps extending beyond quarterly rhythm signals diverted engineering resources.

If Fork #1 = Academic First, Does This Still Trigger?

Probably not. This is the compound effect in action.

When pharma treats you as a research collaborator rather than a vendor, they don’t ask for custom integrations. They want access to the platform methodology and co-authorship credit on publications. Isomorphic’s $2.9B in partnerships are platform access deals, not per-target services contracts.

Fork #1 determines whether Fork #2 even appears. Commercial-first makes services trap very likely. Academic-first makes it unlikely.

For Chai, this fork will become visible in Q1-Q2 2026 if they’ve chosen the commercial path. The first major partnership expansion request will signal which trajectory they’re on.

Fork #3: When a platform company becomes a biotech company without realizing what that means

By Series B (Month 24-30), every drug discovery AI company faces this question: Do we just build the platform, or do we take molecules through clinical trials ourselves?

It shows up as a board discussion, often framed optimistically: “What if we took one of our best antibody candidates into Phase 1? Show pharma what the platform can do. Prove the models work end-to-end.”

The question sounds strategic. It’s actually a referendum on whether the previous two forks went well.

The Two Paths

Platform-only:

License technology to pharma companies

Pharma runs the clinical trials

Revenue: licensing fees, milestone payments, royalties

Capital requirements: moderate ($100-300M total)

Business model: software/SaaS economics

Full-stack (hybrid):

License technology AND run internal clinical pipeline

Chai takes its own molecules into Phase 1/2/3 trials

Revenue: licensing plus potential drug sales if trials succeed

Capital requirements: extreme ($500M-1B+)

Business model: biotech economics

The difference seems like optionality. It’s actually a math problem with one wrong answer.

The Math That Kills Hybrid Models

Platform revenue scale: Even excellent drug discovery AI partnerships generate tens of millions annually. Schrödinger’s drug collaborations, Absci’s milestone payments—this is the realistic range. Call it $20-50M per year at maturity.

Clinical trial costs: A single Phase 3 program routinely exceeds hundreds of millions in annual operational costs. This is before the science—just the administrative overhead, trial site management, regulatory compliance, and patient recruitment.

The gap: Platform revenue of $50M per year cannot fund even one concurrent Phase 3 program that costs $400M per year. And you can’t just run one program—you need portfolio diversification because clinical failure rates are 90%+.

What this means: Full-stack requires continuous external capital raises. You’re never profitable. You’re always fundraising. And if clinical programs don’t hit milestones on investor timelines, you collapse.

The Evidence: No Successful Hybrid Model Yet

Across seven drug discovery AI companies, not one has demonstrated durable hybrid success:

BenevolentAI: Pursued hybrid model aggressively (20+ programs by 2021). When clinical programs didn’t advance fast enough to justify the capital burn, the company collapsed. Down 99%, forced to abandon hybrid and retreat to platform.

Recursion Pharmaceuticals: Running 10+ internal programs plus 10+ partnerships. Raised $680M+ but had to cut programs in 2025 when the capital/milestone math didn’t work.

Insilico Medicine: Filed for Hong Kong IPO but never listed. Raised $110M Series E instead. Burning cash on hybrid model. Platform revenue ($51M in 2023) insufficient for clinical burn rate.

Atomwise: 13 years in, no compounds in clinical trials yet. New CEO hired February 2025 specifically to navigate the transition to hybrid. It’s proving difficult.

The one exception: Isomorphic Labs can afford selective internal programs, but only because they have Alphabet backing and established platform revenue first. Their path was platform economics → then selective internal programs, not hybrid from the start.

Fork #2 Outcome Determines Fork #3 Viability

This is where compound effects become catastrophic:

If you fell into the services trap (Fork #2):

Gross margins already compressed (<70%)

Platform revenue diluted by services

The gap between platform economics and clinical costs gets WIDER

Full-stack becomes a suicide mission

You’re forced into platform-only (if margins recover) or strategic exit (if they don’t)

If you avoided the services trap (Fork #2):

Gross margins strong (>75%)

Platform revenue clean and growing

Partnership terms better (non-exclusive, data sharing from Fork #4)

The gap is still massive, but selective internal programs might be viable

This means 1-2 high-conviction bets, not 10+ portfolio diversification

If you also lost Fork #4 (exclusive data rights):

Even clean platform revenue won’t compound effectively

No network effects, no platform advantages

Each partnership is independent, not reinforcing

Full-stack becomes impossible—no platform leverage to fund it

Forks #2 and #4 together determine whether Fork #3 is even a real choice or just “which exit path do we take?”

Chai’s Position

Chai is 8-12 months away from this fork. The board discussion will happen at Series B, roughly Month 24-30.

If they’ve taken the academic path (Fork #1), avoided the services trap (Fork #2), and retained aggregate learning rights (Fork #4), they might be able to afford one or two disciplined internal programs—proof-of-concept bets funded by platform revenue.

If they’ve taken the commercial path and fallen into the services trap, the internal pipeline discussion will still happen—but it will be driven by investor pressure and the need to show growth, not by strong platform economics. That version ends in capital exhaustion or strategic acquisition.

The fork will be decided by what happened 12-24 months earlier. The board conversation at Series B is really just the moment when earlier decisions become impossible to reverse.

Base Case (60% probability): Commercial → Services → Hybrid Struggle

January 2026 (Month 18):

The partnership Chai has been working on for six months finally closes. Two major pharmaceutical companies sign on. The press releases list dollar figures—expansion from pilot programs to multi-year commitments—and call the relationships “strategic collaborations.” Industry newsletters cover it as validation. The board is pleased.

The contracts, unseen by the public, include language like “exclusive rights to antibody designs for Partner X’s target library” and “dedicated engineering resources for Partner Y’s internal systems.” Nobody outside the company notices yet, but the first irreversible fork just locked in.

March 2026 (Month 20):

A pharma partner calls with a request. They love Chai’s models and want to expand usage across more therapeutic areas. There’s one thing: they need a custom connector to their internal trial management system. The integration is technically straightforward—maybe six weeks of engineering work. They’ve already budgeted for it in the expanded contract terms.

The sales team pushes for it. The revenue is real: an additional $250K annually. The customer is prestigious. It feels like momentum.

Two senior engineers get pulled off platform development to build the integration. The six-week estimate becomes four months. Another partner sees that Chai did custom work for the first partner and requests their own integration. By July, three engineers are maintaining partner-specific code branches instead of improving Chai-2.

Services revenue is now 18% of total revenue. Nobody has announced this publicly. Gross margins slip to 72%, down from 78% at the Series A.

July 2026 (Month 24):

Product release cadence has slowed. Chai-3, originally planned for Q3 2026, slips to Q4, then to “early 2027.” The engineering team is hiring aggressively—headcount up 40% in six months—but not because the platform is scaling. It’s because maintaining three custom deployment branches is labor-intensive.

Senior platform engineers begin leaving. Two depart in the past quarter for competitors.

The board starts discussing what’s next. Platform revenue is steady—$8M annualized—but it’s not venture-scale growth. Someone suggests: “What if we took one of our best antibody candidates through preclinical ourselves? Show pharma what the platform can do.”

The idea takes hold. Internal pipeline conversations begin.

January 2027 (Month 30):

Series B closes at $200M. The valuation multiple is mid-range—below what pure software platforms command—but investors see the partnerships as validation. Chai announces two internal drug candidates that will enter preclinical development. The press coverage frames this as evolution: “AI platform company becomes AI-powered biotech.”

The services trap is now locked in. The hybrid model is now locked in. And the clock is ticking.

July 2027 (Month 36):

The two internal programs are consuming capital faster than projected. Preclinical work for antibody therapies requires extensive validation, manufacturing partnerships, and regulatory preparation. Each program burns $3-5M per quarter before even reaching Phase 1.

Platform partnerships are steady but insufficient. Annual platform revenue is around $15-20M—not enough to fund clinical programs. The company is dependent on continuous capital raises. The Series C will need to happen by mid-2028.

Board conversations quietly shift to “strategic options.” The company that could have become the infrastructure layer for protein design is now choosing between:

Acquisition by a pharmaceutical company or life sciences consultancy ($300-500M range)

Continuous capital raises to fund the hybrid model, with no clear path to profitability

Abandoning the internal pipeline and retreating to pure platform (which would require writing down millions and likely losing key team members)

One early fork—commercial velocity over academic credibility—created a sequence that became irreversible. Services revenue funded a hybrid strategy that looked like optionality but was actually a capital trap.

Primary observables supporting this path:

Partnership announcements in early 2026 include “exclusive” or “dedicated” language

Engineering hiring accelerates faster than customer growth (40%+ headcount growth in first half of 2026)

Services/implementation revenue disclosed or implied above 15% by mid-2026

Product release cadence slows (Chai-3 delayed beyond original timeline)

Internal pipeline announcement (2-3 programs) by early 2027

Series B raise in mid-range multiple territory despite partnerships

Bull Case (25% probability): Academic → Platform → Selective Internal

January 2026 (Month 18):

A paper appears in Nature. The title: “Chai-2: Scalable AI-Driven Antibody Design with 20% De Novo Success Rates.” The author list includes Chai’s founders alongside researchers from three independent academic labs—MIT, Stanford, and the Scripps Research Institute—who validated the results using their own datasets.

The paper doesn’t just describe Chai’s models. It shows that external teams, using publicly available Chai-1 components, successfully designed functional antibodies for novel targets. Independent validation. Reproducible results. The kind of scientific credibility that shifts perception.

Within weeks, pharmaceutical companies that had been waiting for proof-of-concept reach out. But the conversations are different from typical vendor pitches. They’re asking about research collaborations, joint publications, and platform access—not about custom integrations for their specific workflows.

March 2026 (Month 20):

Two partnerships close. Both are structured as non-exclusive platform access agreements. Pharma companies pay for compute and API calls, not per-target licensing. The contracts include explicit clauses allowing Chai to use de-identified, aggregate data to improve the base models. Joint publication rights are standard.

One partner—a top-5 pharmaceutical company—requests a technical deep-dive session. They want to understand Chai’s model architecture, not because they’re evaluating a purchase, but because they’re considering citing it in their own research publications. The relationship is peer-to-peer.

A senior engineer who had been at a competitive AI-drug-discovery company joins Chai. In interviews, he mentions that he left because his previous company had him maintaining three custom deployment branches for different pharma customers. “Here, we’re building platform infrastructure,” he says. “The work compounds.”

July 2026 (Month 24):

Chai-2.1 ships on schedule. The release includes improvements to binding affinity prediction and a new module for antibody humanization. These features came from aggregate learnings across multiple partnerships—each collaboration made the platform better for everyone.

Platform revenue is growing faster than engineering headcount. Services revenue stays below 10%—mostly implementation support that Chai deliberately prices high to discourage demand. Gross margins remain above 80%.

The engineering team posts a job opening: “Research Scientist - Protein Design.” The description emphasizes publications, open-source contributions, and research impact. This isn’t a customer-facing role. It’s platform depth.

January 2027 (Month 30):

Series B closes at $150M with a high-teens revenue multiple. The investor deck emphasizes platform economics: 82% gross margins, 3x year-over-year revenue growth, seven pharmaceutical partnerships on non-exclusive terms, and a clear path to $50M+ annual platform revenue within 18 months.

At the same board meeting, Chai announces one internal drug candidate: a monoclonal antibody for a rare autoimmune disorder. The target was chosen carefully. It’s scientifically interesting, clinically tractable, and won’t require competing directly with Big Pharma for years. This isn’t a portfolio strategy—it’s a proof-of-concept designed to show that Chai’s platform can take molecules from design to clinic.

The internal program has a dedicated team of four people: one research lead, one translational scientist, and two project managers. Not twenty people. Not five programs. One high-conviction bet.

July 2027 (Month 36):

Platform revenue hits $22M annualized, up from $8M eighteen months earlier. Ten pharmaceutical and biotech companies now use Chai’s platform. Three have published papers crediting Chai’s models. Academic labs continue to validate results independently, and two universities have licensed Chai-1 for teaching computational biology courses.

The internal antibody candidate enters IND-enabling studies. Preclinical data looks strong. Chai will file an IND by year-end and enter Phase 1 in early 2028. The program has cost $6M to date—fully funded by platform revenue.

A second internal program begins: another rare-disease target, same disciplined approach. The company can afford selective bets because the platform business is working. Revenue funds research. Research improves the platform. The platform attracts better partnerships.

Gross margins stay above 80%. Engineering turnover is low. Product velocity remains high—Chai-3 is on track for late 2027 release.

Board conversations are about market positioning, not survival. Should Chai expand into enzyme design? Should they open a Europe office? What does a $3B outcome look like in five years?

The company that took the academic path first isn’t racing toward an exit. It’s building toward category ownership.

Primary observables supporting this path:

Major peer-reviewed publication (Nature, Science, Cell) with independent validation by Q1 2026

Partnership announcements emphasize “research collaboration,” “platform access,” “joint publications”

Partnership terms allow Chai to retain aggregate learning rights (detected through publication clauses and non-exclusive language)

Engineering hiring focused on research/platform roles, not customer-facing implementation

Platform releases maintain quarterly cadence through 2026

Services revenue stays below 15% (if disclosed)

Series B at high-teens multiple despite slower absolute dollar growth

Internal pipeline limited to 1-2 highly selective programs (not 5+)

Academic labs publish independent validations citing Chai models

Specific falsification criterion: If Chai publishes a major peer-reviewed paper with independent validation AND partnership terms include explicit publication clauses by March 2026, Bull Case probability increases significantly. If no major publication appears by March 2026, Bull Case probability drops toward zero.

Bear Case (15% probability): Commercial → Services → Quick Exit

January 2026 (Month 18):

Three partnership announcements in six weeks. Each press release emphasizes scale and speed: “strategic collaboration,” “dedicated engineering resources,” “exclusive focus on Partner X’s oncology portfolio.” The dollar figures are impressive—$2.5M in new annual commitments.

The press releases never mention the legal details: each contract includes per-target licensing terms and requirements for Partner-specific model fine-tuning. The language commits Chai to maintaining separate deployments for each partner’s proprietary data environments.

The board celebrates the partnerships as validation. Revenue projections for the year double. Sales targets get more aggressive.

March 2026 (Month 20):

All three partners request custom integration work within the same month. One wants a connector to their legacy trial management system. Another needs Partner-specific antibody humanization algorithms. The third requests a custom dashboard for their internal R&D teams.

Each project is scoped at 4-6 weeks. Each takes three months. By June, five engineers—nearly 40% of the engineering team—are working full-time on Partner-specific implementations. None of this work improves the core platform.

Chai posts two job openings: “Professional Services Manager” and “Forward Deployed Engineer.” The descriptions emphasize “customer success,” “on-site support,” and “rapid implementation.” These aren’t research roles.

Services revenue hits 28% of total by the end of Q2. Gross margins compress to 62%. Nobody has publicly disclosed this yet, but the Series B investors who are conducting diligence can see it in the data room.

July 2026 (Month 24):

Chai-3, originally scheduled for Q2 release, is now “under development with no set timeline.” The platform engineering team has shrunk—not through layoffs, but through departures. Two senior engineers left for competitors in the past quarter.

The three partnerships are generating revenue, but they’re not leading to platform expansion. Each pharma company treats Chai as a services vendor, not a technology platform. When one partner asks if Chai can take on additional custom development work, the answer is yes—because the revenue is needed.

Series B conversations begin, but investor feedback is consistent: “The margins look like a consulting firm, not a software company.” Term sheets come in at mid-to-low single-digit revenue multiples—far below what comparable platform companies command. One VC passes with a note: “Great tech, but we’re concerned about the business model trajectory.”

January 2027 (Month 30):

Chai’s board receives an acquisition offer from a large life sciences consultancy. The price is $280M—a respectable outcome for early investors, but not the venture-scale exit the company could have achieved.

The acquirer’s thesis is straightforward: Chai’s technology fits into their existing pharmaceutical services business. The models will become part of a broader suite of drug discovery consulting offerings. The engineering team will integrate into the acquirer’s R&D services division.

The board debates for three weeks. The alternative is raising a difficult Series B at compressed multiples and trying to reverse course—retreating from services, rebuilding the platform team, restructuring the partnerships. It’s theoretically possible but would require writing down millions in partner commitments and likely losing more engineering talent.

The acquisition closes in March 2027. The press release frames it as strategic: “Leading AI drug discovery technology joins global life sciences leader.” The platform dreams ended eighteen months earlier, when the first partnership included the phrase “dedicated engineering resources.”

The technology was never the constraint. The execution fork was.

Primary observables:

Three or more partnership announcements within Q4 2025 - Q1 2026, all with “strategic,” “dedicated,” or “exclusive” language

Job postings for “Professional Services Manager,” “Forward Deployed Engineer,” or similar client-facing implementation roles by Q1 2026

No major platform releases (Chai-3) throughout 2026

Engineering departures visible via LinkedIn (senior engineers moving to competitors)

Series B rumors circulating at compressed multiples or stalling entirely

Acquisition rumors by late 2026

Acquisition announcement by Q1 2027 at $200-400M valuation

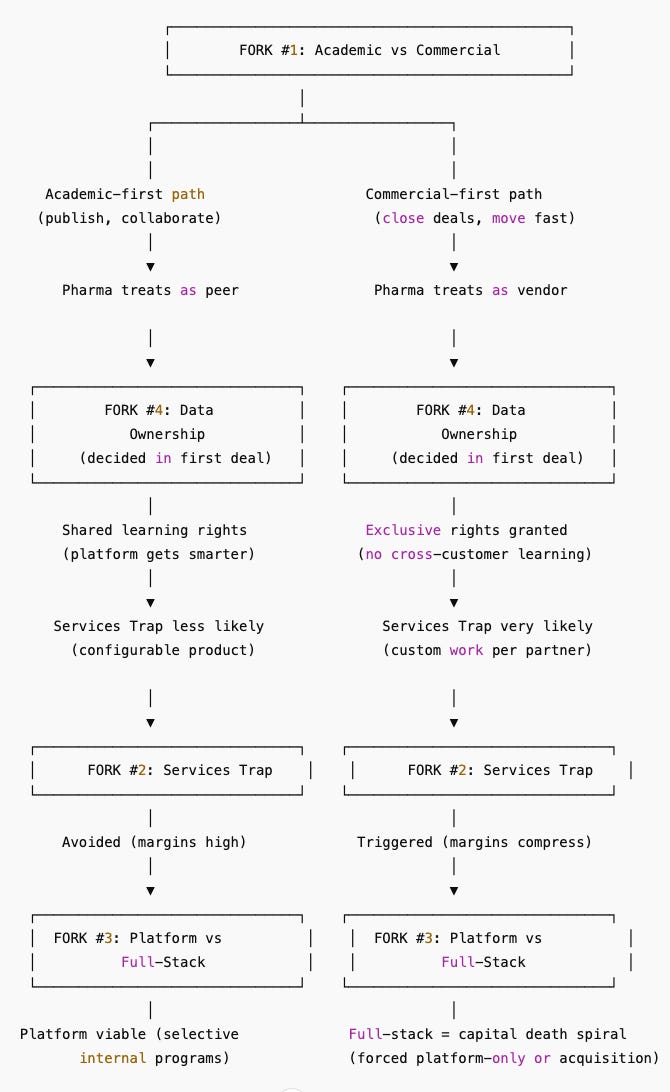

The Cascade: How Forks Compound

If this feels like one decision limiting the next, that’s because it is. Here’s how they connect:

Fig. 1: Once Fork #4 is decided, the remaining forks are almost impossible to reverse.

One choice determines the next. And three of the four can’t be undone.

Here’s how they connect:

Fork #1 determines Fork #4:

Academic credibility → pharma treats you as research peer → shared learning rights negotiated from strength

Commercial velocity → pharma treats you as vendor → exclusive rights demanded as standard practice

Fork #4 determines Fork #2:

Shared learning rights → platform can compound across customers → services trap avoidable with discipline

Exclusive rights → per-customer customization required → services trap becomes very likely

Forks #2 + #4 together determine Fork #3:

Avoided services trap AND retained learning rights → platform economics strong → can afford selective internal programs (1-2, not 10+)

Fell into services trap OR gave away learning rights → platform economics broken → full-stack becomes capital death spiral

The path becomes effectively irreversible after Fork #4. Once you’ve granted exclusive data rights in your first major partnership, every subsequent partnership expects the same terms. Once you’ve accepted customization work, more customization requests follow. By the time you reach Fork #3, you’re not choosing a strategy—you’re discovering which path the earlier forks already locked in.

Early decisions constrain later options. That’s what makes them forks.

What to Watch: Observable Signals

All indicators are inferable from public announcements, hiring data, and disclosed metrics—no insider information required.

January 2026 (Month 18): Fork #1 Resolution

Academic Path Signals:

Major peer-reviewed paper in Nature, Science, or Cell

Independent validation by external labs (MIT, Stanford, academic institutions)

Partnership announcements emphasize “research collaboration,” “platform access,” “joint publications”

Hiring: Research scientists, platform engineers

Partnership language includes publication clauses

Commercial Path Signals:

Publication cadence slows or stops after Series A

Partnership announcements use “strategic partnership,” “dedicated team,” “exclusive access”

Hiring: Client-facing roles, implementation engineers, customer success

No publication clauses mentioned in partnership terms

→ Decisive signal: Partnership language. If announcements use “exclusive,” “dedicated,” or “per-target,” commercial path confirmed.

April 2026 (Month 20): Fork #4 + Early Fork #2 Signals

Shared Learning Rights (Platform Path):

“Non-exclusive collaboration” language in announcements

Multiple partnerships in overlapping therapeutic areas (suggests shared learning)

Compute/API-based pricing mentioned (not per-target)

Joint publications announced or referenced

Exclusive Rights (Services Path):

“Dedicated to Partner X’s programs” or similar exclusive language

Per-target or per-molecule licensing structure implied

No mention of shared learning or publications

Job postings for “Professional Services Manager” or “Forward Deployed Engineer”

July 2026 (Month 24): Fork #2 Resolution

Avoided Services Trap:

Gross margins consistently above 75% (if disclosed)

Services/implementation revenue <15%

Platform engineering headcount stable relative to customer count

Regular product releases maintained (quarterly cadence)

Fell Into Services Trap:

Gross margins <70% or declining trend

Services revenue >20% and growing

Job postings: “Professional Services Manager,” “Forward Deployed Engineers”

Product roadmap slips—long gaps between major releases

Engineering departures visible on LinkedIn

→ Decisive signal: Revenue mix. If services/implementation >20% of disclosed or implied revenue, services trap confirmed.

January 2027 (Month 30): Fork #3 Resolution

Platform Focus:

Series B at high-teens revenue multiple (if disclosed/reported)

0-2 internal programs announced (highly selective)

Capital raise: $100-200M range

Announcements emphasize “platform expansion,” “research partnerships”

Continued hiring: platform engineers, research scientists

Hybrid Model:

Series B at mid-to-low single-digit multiple or acquisition conversations

5+ internal programs announced

Capital raise: $250M+ (or acquisition instead)

Announcements emphasize “pipeline development,” “internal programs,” “clinical candidates”

Hiring shifts: clinical operations, regulatory affairs, program managers

→ Decisive signal: Internal pipeline size. If 5+ programs announced, hybrid model confirmed.

Check-Back: October 2026

By October 2026 (Month 30), we’ll have enough data to evaluate:

Which path Chai took at each fork

Whether compound effects materialized as predicted

Whether timing windows held

Observable signals that indicated the path

What the analysis got right and what it got wrong

Every prediction in this piece is falsifiable. Every outcome will be documented.

Methodology Notes

How This Analysis Was Conducted

Research approach: This analysis draws from seven drug discovery AI companies—nearly a complete census of major public or well-funded private players in this specific vertical. Company research used publicly available information only: SEC filings, press releases, published papers, hiring data via LinkedIn, industry reports, and news coverage.

Sample size disclaimer: Seven companies is a small sample. The pattern observed may be specific to drug discovery AI and may not generalize to other AI verticals. Drug discovery faces unique challenges (regulatory requirements, capital intensity, long clinical timelines) that may not apply elsewhere.

Confidence calibration: Predictions carry 60-70% confidence because Chai is at Month 21 (mid-stage execution) where observable signals are strong but multiple variables remain in motion. This is lower than the 85-95% certainty possible for earlier architectural decisions (Month 0-12) but higher than late-stage scaling predictions (Month 36+) where external factors dominate.

The compound cascade (Fork #1 → #4 → #2 → #3) adds uncertainty at each step. Each downstream fork depends on upstream outcomes plus new external factors (partnership negotiations, market conditions, competitive dynamics).

Timing windows:

Fork #1: Month 14-21 (happening now for Chai)

Fork #4: Month 15-20 (embedded in first major partnerships)

Fork #2: Month 18-24 (if commercial path chosen)

Fork #3: Month 24-30 (Series B timing)

These windows reflect patterns observed across the seven-company sample but may not hold precisely for individual cases.

Falsification Criteria

Fork timing failures:

Fork #1 already decided before Month 14 (too late to predict)

Fork #2 triggers at Month 10-12 or Month 26+ (timing window wrong)

Fork #3 decision happens before Series B (earlier than expected)

Mechanism failures:

Fork #1 = Commercial but Fork #2 never triggers (pharma doesn’t request customization)

Fork #2 = Services trap but margins stay >75% (services economics work differently than predicted)

Fork #3 = Full-stack but capital requirements prove manageable (clinical trials cheaper than estimated)

Outcome failures:

Hybrid model succeeds spectacularly (first drug discovery AI company to do so sustainably)

Platform-only model fails due to insufficient revenue despite clean economics

Different failure mode entirely (technology doesn’t work, market doesn’t materialize, regulatory blockers)

Sector-specific exceptions:

Drug discovery AI actually requires customization for regulatory compliance (pattern doesn’t apply)

Chai has already solved fork challenges through novel approaches not visible in public data

Alphabet or similar strategic acquirer changes path dependencies entirely

Limitations

What this analysis cannot see:

Internal unit economics, pipeline health, or team dynamics

Actual contract terms (data ownership clauses are inferred from secondary signals)

Board conversations or strategic debates happening privately

Technical capabilities or limitations of Chai’s models beyond published hit rates

What could change predictions:

Macroeconomic conditions affecting funding availability

Regulatory changes in drug approval processes

Competitive dynamics or technological breakthroughs

Key personnel changes or team departures

Strategic partnerships or acquisitions not yet announced

Epistemic Honesty

This is pattern research testing whether execution forks are predictable from public signals. It is not investment advice, due diligence, or comprehensive company analysis. The predictions are falsifiable and will be evaluated publicly in October 2026—right or wrong.

If the pattern holds (70%+ accuracy across predictions), it suggests execution forks in startups may be more systematic than commonly assumed. If predictions fail, either the patterns don’t exist, the timing windows are wrong, or the sector-specific factors are too strong.

References

[1] Nobel Prize Committee. (2024). “The Nobel Prize in Chemistry 2024.” https://www.nobelprize.org/prizes/chemistry/2024/summary/

[2] Chai Discovery. (2024). “Chai-1: Decoding the molecular interactions of life.” bioRxiv preprint.

https://www.biorxiv.org/content/10.1101/2024.10.10.615955v1

[3] Business Wire. (2025). “Chai Discovery Announces $70 million Series A To Transform Molecular Design.” August 6, 2025. https://www.businesswire.com/news/home/20250806670137/en/Chai-Discovery-Announces-$70-million-Series-A-To-Transform-Molecular-Design

[4] Built In San Francisco. (2025). “AI Molecular Design Startup Chai Discovery Secures $70M Series A.” August 8, 2025.

https://www.builtinsf.com/articles/chai-discovery-secures-70m-series-a-20250808

[5] MedPath. (2025). “Chai Discovery Raises $70M Series A to Revolutionize Antibody Design with AI Platform, Achieving 20% Hit Rate.” https://trial.medpath.com/news/12880e3c0f8503cf/chai-discovery-raises-70m-series-a-to-revolutionize-antibody-design-with-ai-platform-achieving-20-hit-rate

[6] Business Wire. (2025). “Chai Discovery Announces $70 million Series A To Transform Molecular Design” (includes Mikael Dolsten board appointment). August 6, 2025.

https://www.businesswire.com/news/home/20250806670137/en/Chai-Discovery-Announces-$70-million-Series-A-To-Transform-Molecular-Design

[7] BenevolentAI. (2025). “EGM Results announcement - Delisting from Euronext Amsterdam effective 13 March 2025.” March 12, 2025. https://www.benevolent.com/news-and-media/press-releases-and-in-media/egm-results-announcement/

[8] Recursion Pharmaceuticals. (2025). “Recursion Reports First Quarter 2025 Financial Results and Provides Business Update” (program deprioritization announcement). May 5, 2025.

https://ir.recursion.com/news-releases/news-release-details/recursion-reports-first-quarter-2025-financial-results-and

[9] Atomwise. (2025). “Atomwise Appoints Steve Worland, Ph.D. as Chief Executive Officer.” February 18, 2025. https://www.atomwise.com/2025/02/18/atomwise-appoints-steve-worland-ph-d-as-chief-executive-officer/

[10] Genetic Engineering News. (2025). “Insilico Medicine raises $110M Series E; IPO plans delayed.”

https://www.genengnews.com/news/insilico-medicine-raises-110m-series-e/

[11] Isomorphic Labs. (2024). Partnership announcements:

“Isomorphic Labs to Receive $45 Million in Upfront Payment For Multi-Target Research Collaborations with Lilly.” January 7, 2024. https://www.isomorphiclabs.com/articles/isomorphic-labs-kicks-off-2024-with-two-pharmaceutical-collaborations

“Isomorphic Labs to Receive $37.5 Million Upfront Payment From Novartis.” January 7, 2024.

https://www.prnewswire.com/news-releases/isomorphic-labs-announces-strategic-multi-target-research-collaboration-with-novartis-302027387.htmlCombined deal value: $2.9B ($1.7B + $1.2B in potential milestone payments plus upfront payments)

[12] Schrödinger Corporation. (2023-2024). Investor relations materials and SEC filings. Revenue composition and business model disclosures available at https://investors.schrodinger.com

[13] Absci Corporation. (2021-2024). SEC filings (Form S-1, 10-K, 10-Q). Business model and partnership structure.

https://investors.absci.com

[14] Benchmarkit. (2024). “2024 SaaS Performance Metrics.” https://www.benchmarkit.ai/2024benchmarks

[15] Stay SaaSy. (2022). “How to Improve Your Gross Margins.” https://staysaasy.com/product/2022/06/12/how-to-improve-your-gross-margins.html

This analysis is based on publicly available information as of December 2025. This is pattern research testing whether execution forks are predictable from public signals. It is not investment advice. Predictions will be evaluated October 2026.

Pattern tracking:

Pattern #1: Research Grid (Month 11) - Services trap prediction - Check-back April 2026

Pattern #2: DatologyAI (Month 25) - Services trap verification - Check-back October 2026

Pattern #3: Chai Discovery (Month 20) - Compound fork effects - Check-back October 2026

Pattern #4

Flux (Month 29) - GTM lock-in - Check back Jan 2027